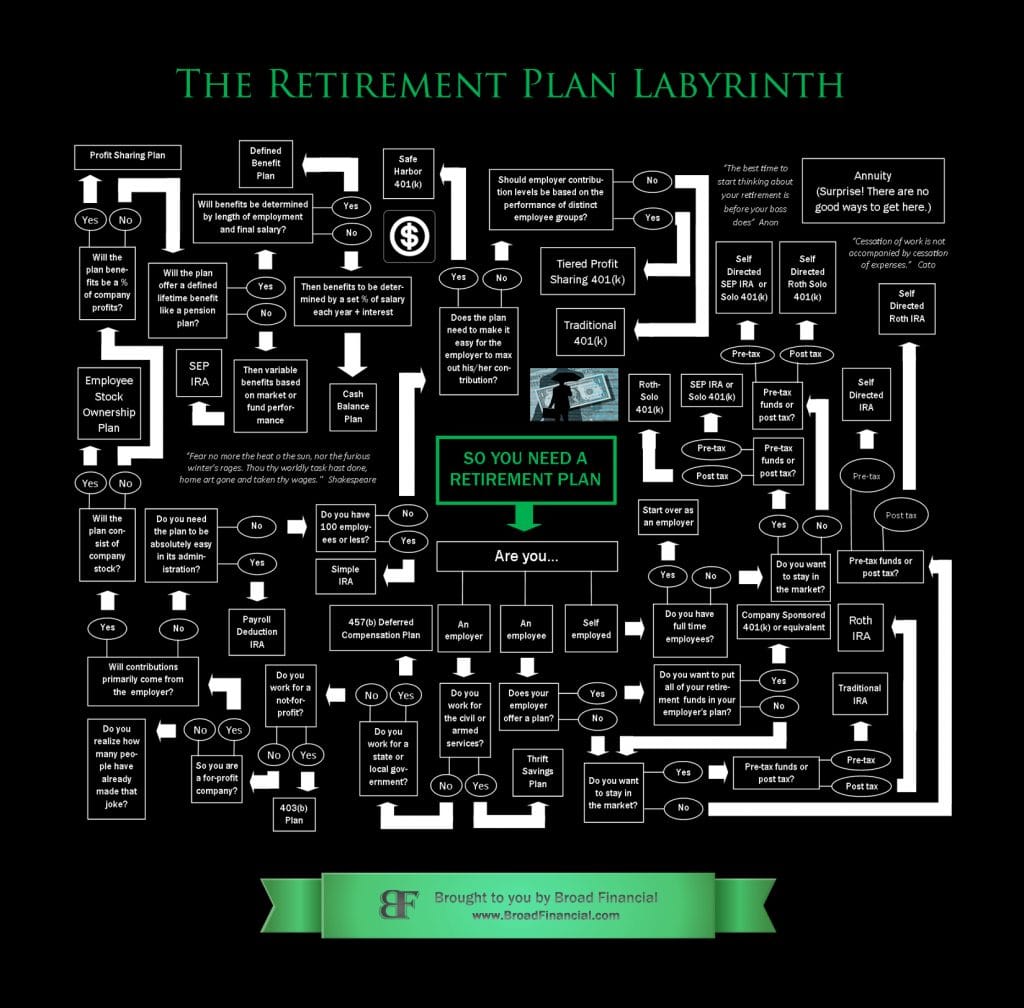

There’s a reason that thinking about retirement planning makes you feel like a 3rd grader trying to understand nuclear physics: it’s complicated, there are a lot of variables, and one wrong move can mean financial armageddon. Even with a simplified options map, you can quickly get lost in the thicket. Try your luck and we’ll meet back on the other side.

Here are the terms you need to know to find your way around the retirement labyrinth.

IRA – An IRA (Individual Retirement Account) is the standard model retirement platform. An individual can contribute up to $7,000 from his/her annual income towards retirement savings ($8,000 if age 50+). The government has incentivized this contribution by offering the account holder a tax benefit. Any money contributed will be tax deferred, i.e. the account holder will not have to pay taxes on that money until retirement. This usually comes out to a reduction of the tax payment because the retiring individual is in a lower tax bracket.

401(k) – A 401(k) is a type of retirement account that is commonly used by employers. It offers the same tax deferred benefits as an IRA, but it comes with two distinct advantages. The first is an elevated contribution limit. While the IRA contribution limit is currently (2024) $7,000 ($8,000 if age 50+), the potential contribution limit for the 401(k) is $69,000 ($76,500 if age 50+). The second advantage is the possibility of an employer contribution. Employers will sometimes offer matching contributions to employees as an incentive to attract top notch talent, as well as to take advantage of applicable deductions.

Roth – There are two ways that retirement investors can receive a tax benefit for their contributions. The traditional way is to contribute pre-tax dollars to the retirement account and pay the lower tax rate later. The second way is to contribute post tax dollars, i.e. contribute income for which you’ve already paid taxes, and then allow it to grow tax free. A retirement account that takes post tax dollars is known as a Roth. Whether an investor should choose traditional or Roth depends on a number of factors including current tax bracket and investment potential.

Self Direction – The majority of retirement funds are invested in market products like mutual funds or diversified stock portfolios. The allocation of the funds are determined by the mutual fund administrator or by a Wall Street professional. Self direction refers to an investor taking control of his/her retirement funds and placing them in assets of their own choosing. Investors often choose this strategy when they have an asset they would like to invest in (e.g. a specific piece of real estate) but are unable to do through the standard channels.

Solo 401(k) – As mentioned above, the 401(k) offers significant advantages over an IRA, but it does so only for company employees. The Solo 401(k) extends those benefits to self employed individuals.

Profit Sharing – A Profit Sharing plan is a company sponsored retirement plan where contributions are made at the employer’s discretion, and are often based on the company’s profit levels. It offers employers flexibility as they can determine not only the level of contributions, but also how they should be distributed amongst the company hierarchy.

Defined Benefit – A Defined Benefit plan makes set contributions based upon factors such as salary history and current length of employment. Since the benefits are formulaic (and not dependent upon profits) this is a great plan to attract employees. Also, this plan often allows employers to contribute more than in other plans, thereby making it a good option for companies that want to max out their tax-deductible contributions.

Annuity – An annuity is a type of insurance product where the investor makes contributions, and in return receives a series of future payments. The payments can be in the form of a lump sum or spaced out as retirement income. The amount of the payments are also variable as they can be fixed or dependent upon investment return. Annuities are notorious for their high fees and inflexibility once you invest in them.

Address:

One Paragon Drive

Suite 270

Montvale, NJ 07645

Phone: (800) 395-5200

Mondays – Thursdays: 8:00 am – 6:00 pm EST

Fridays – 10:00 am – 4:00 pm EST