Tax code can be confusing but that shouldn’t stop you from getting the maximum benefit. Let’s break down a recent tax change involving the new Solo 401(k) deadline and clarify what it means for you. (If you happen to enjoy tax law in all of its glorious complexity, you can check out the original Congressional bill here. Pay particular attention to Sec. 201.)

The Solo 401(k) is a little bit trickier than other self-directed plans because it involves two different kinds of contributions. The first is the Salary Deferral contribution. This is equivalent to the employee contribution that you would find in a standard 401(k). The second is the Profit Sharing contribution. This is similar to the employer contribution. What makes the Solo 401(k) unique is that it contains both elements at once, and the Solo plan participant manages both at the same time. (A Broad Specialist can help you navigate this process if you have questions.)

The easiest way to understand the new Solo 401(k) guidelines is to remember three things:

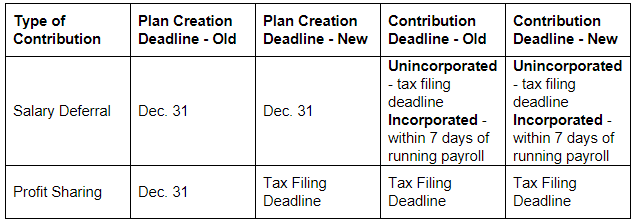

Now let's take a look at the two types of contributions. The Salary Deferral contribution was not changed under the new guidelines. In order to make a Salary Deferral contribution, the Solo 401(k) plan must be created by December 31. The contribution deadline is variable. If your plan is sponsored by an incorporated entity, then contributions must be made within seven days of running payroll. If it is unincorporated, then you have until the tax filing deadline (with all applicable extensions) to make your contribution. The Profit Sharing contribution was changed under the new guidelines. Now both the Plan Creation deadline and the Contribution deadline are the same as the tax filing deadline. Here’s a chart to help visualize the current guidelines. Note that only one deadline has changed with the new rules: the Profit Sharing Plan Creation deadline. Table 1: Solo 401(k) Guidelines

The Solo 401(k) changes have different implications depending on where you’re holding in the investing process.

Does 2020 have new contribution limits for the Solo 401(k)?

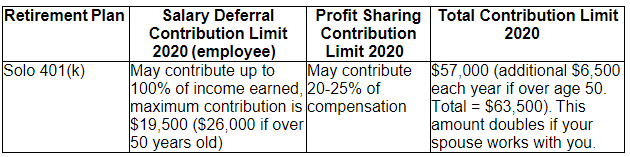

The contribution limits have gone up slightly. Here’s a break down:

Table 2: Solo 401(k) Contribution Limits 2020

Source: https://www.irs.gov/retirement-plans/one-participant-401k-plans

How do I calculate my contribution limit?

Calculating your contribution limit is a simple three-step equation. For example, if you make $50,000 income from your self-employed business, you can contribute up to $32,000 to your Solo 401(k).

To calculate, complete the following:

To determine your personal contribution limit, refer to the Solo 401(k) Calculator.

Can I receive a loan from my Solo 401(k)?

Yes! You may borrow up to $50,000 from your Solo 401(k) to use however you like. Learn more about taking a loan from your Solo 401(k) and the repayment structure.

For any additional questions, contact a Self Directed Expert.

Address:

One Paragon Drive

Suite 270

Montvale, NJ 07645

Phone: (800) 395-5200

Mondays – Thursdays: 8:00 am – 6:00 pm EST

Fridays – 10:00 am – 4:00 pm EST